Index Universal Life

Insurance

A vehicle that helps you build predictable, safe, tax-efficient wealth for the rest of your life.

Key Benefits

Stead growth without risk, Protection from "what ifs" and Securing your Financial Future by Tax-Efficient Savings

Safe & Steady Growth

Cash Value participates in gains without LOSING your principal balance.

Steady growth with an average 6% - 9% yearly gains (some uncapped) and downside protection from losses, a floor of 0%. Based on the returns of an Index like the S&P 500.

Life Long Protection

Permanent coverage with the option to protect you and your family all your life.

Built in living benefits for critical, chronic and terminal illnesses. Covers you in case of heart attack, stroke and cancer. Insurance that work for you when you are live and healthy!

Tax-Efficient And Flexibility

Cash Value principal grows Tax-Free and Tax-Free access.

As your cash value balance continues to grow yearly without loss, you can also have Tax-Free access to your balance at anytime through policy loans.

Gives your more flexibility and control.

Steady returns and

long-lasting protection

Index-linked returns provide the potential for stronger cash value growth compared to other stable alternatives like fixed policies, bank savings or CDs. This gives you market upside in up years.

Floor rate shields your cash value from any market losses in down years, providing stability and preserving your principal all life long while providing the benefits of Life Insurance and living benefits comparable to long-term care.

Index Universal Life Insurance FAQs

Many have questions regarding an Index Universal Life, so to help our clients understand its value we have compiled a list of questions to help our clients!

Hope this helps you!

What is an Index Universal Life Insurance?

Index Universal Life Insurance (IUL) is a type of permanent life insurance that builds cash value based on the performance of a market index, like the S&P 500. It provides lifetime protection along with the potential for cash value growth linked to the index.

Who should consider buying Index Universal Life Insurance?

IUL is a good option for people who want lifetime protection, tax-advantaged growth potential, and flexibility to access cash value if needed in the future. It provides valuable benefits beyond just a death benefit.

How does the cash value grow in an IUL policy?

The cash value in an IUL policy grows in two ways - through guaranteed interest payments credited by the insurance company and through indexed returns based on the performance of the selected market index. Indexed returns are credited to your cash value when the market Index goes up.

What is the benefit of growing cash value inside an IUL policy?

There are many benefits of growing cash value inside an Index Universal Life Insurance Policy, including:

Upside Potential - The index-linked returns provide the potential for stronger cash value growth compared to other stable alternatives like fixed UL policies, bank savings or CDs. This gives you market upside in up years.

Downside Protection - The floor rate shields your cash value from any market losses in down years, providing stability and preserving your principal. If the index performs poorly and has a negative return for the year, your cash value is protected by the floor rate (i.e 0%). You won't lose any money, but you won't earn any interest for that year either.

Flexible Access - You can withdraw or borrow from your cash value later in life for supplemental retirement income or other financial needs. This access is generally tax-free.

What are the Tax Benefits of an IUL policy?

IUL provides tax-deferred growth potential on your cash value. Loans and withdrawals can also be taken out tax-free up to your cost basis amount. Proceeds paid to beneficiaries are income tax-free.

How are premiums and death benefits determined?

You choose a guaranteed death benefit, pay a target premium which covers costs, and the rest goes towards building cash value. You can also pay more to build cash faster or less if you need to adjust your budget. So in other words you get to control the policy. Our expert financial professional can help you structure the right policy to fit your needs.

Why an IUL might be for you

Here are some of the examples of our clients we have helped in the past

How would an IUL fit for parents and grandparents?

Index Universal Life Insurance (IUL) is a type of permanent life insurance that builds cash value based on the performance of a market index, like the S&P 500. It provides lifetime protection along with the potential for cash value growth linked to the index.

Who should consider buying Index Universal Life Insurance?

IUL is a good option for people who want lifetime protection, tax-advantaged growth potential, and flexibility to access cash value if needed in the future. It provides valuable benefits beyond just a death benefit.

Why might parents choose an IUL over a 529 savings plan?

While both IUL and 529 plans both have great advantages for securing your child's financial future. Here are some reasons why some of our clients who are parents chose an IUL over 529 plans:

529 balances reduce need-based financial aid eligibility, while IUL cash values have no impact.

Withdrawals from 529 plans count as student income and reduce aid. IUL loans do not.

Remaining 529 money after college is taxed if not used for education. IUL cash can be used tax-free for anything.

IUL allows tax-free access to cash for college without harming aid eligibility.

Kids can use IUL loans rather than parent PLUS loans, avoiding debt in the parents' names.

IUL gives families more options to pay tuition in the most tax-efficient way.

Overall, the financial aid flexibility of accessing cash from an IUL without penalty makes it very appealing versus tying up money in a 529 that can negatively impact aid. Families can optimize aid and taxes.

Parents / Grandparents

As first-time parents, ensuring your newborn child is protected is top priority. An IUL policy from birth can provide lifelong insurance coverage along with a nest egg that can one day help fund college or other needs.

Retirement Planning

Planning for retirement it is always better to plan early than waiting till you're 35 or older. Index Universal Life insurance policy can complement your retirement planning and provide funds to support your lifestyle into your later years. Tax-free access to cash value can help cover gaps left by IRAs and pensions.

How an IUL can be used for Retirement Income?

The ability to grow supplemental funds tax-deferred and access them tax-free in retirement makes an Index Universal Life insurance policy a very efficient vehicle for supplementing traditional retirement accounts. Its flexibility and upside potential help optimize overall retirement income.

How can an IUL help avoid taxes on Social Security & IRA Withdrawals?

Many retirees end up with higher overall income than they expected due to required minimum distributions from IRAs plus Social Security benefits. This can result in taxation of up to 85% of Social Security and increased taxation on IRA withdrawals. With an IUL policy, retirees can take tax-free loans or withdrawals from cash value to help fill income gaps, avoiding additional taxation. This maximizes tax efficiency in retirement.

How an IUL can be used for tax-free retirement funds with long-term care alternative?

One of the key advantages of an Index Universal Life insurance policy is that it provides lifetime coverage. Unlike term insurance, an IUL policy is permanent and lasts your entire life as long as you pay the premiums.

This permanent nature makes IUL a strong retirement planning tool. It can provide tax-advantaged growth on a long-term basis to fund your retirement years. The policy will be there through your retirement providing tax-free access to cash value if needed.

And the permanent coverage and it's "living benefits" feature of an IUL policy means benefits continue if you were to need long-term care later in retirement. The death benefit and cash value don't go away if you get sick or develop chronic conditions. This can help pay for potential long-term care costs.

How can an IUL help retain key employees while increasing tax deductions?

An IUL can be used to help business owners decrease tax liabilities. There is a way to structure an IUL policy where your business can enjoy tax deductions while the policy provides tax-advantaged benefits for both the company and the individual insured. This arrangement can be highly tax-efficient while providing key person protection and supplementing retirement.

How can an IUL help with Executive Bonus Plans?

An executive bonus plan allows a business to purchase a life insurance policy on a key executive and deduct the premiums as a business expense. The company owns the policy during employment, while the executive receives tax-favored benefits.

An IUL is well-suited for executive bonus plans because:

Premiums paid by the company are tax deductible as a business expense.

The death benefit is received income tax-free by the company if the executive passes away.

The business can access the cash value via tax-free policy loans for liquidity needs.

The insured executive has no taxable income on the premium payments or cash value growth.

At retirement, the executive can take individual ownership of the policy from the business with no tax impact.

Owner Tax-Efficient Retirement Plan

Business owners can get an IUL policy to create tax free income for themselves while also decreasing tax liabilities with an IUL.

Their business entity funds the premium and can be the owner of the policy while they are the an insured.

Premiums are tax-deductible as business expense while the policy cash value grows tax-deferred and can be accessed via tax-free policy loans by the business for opportunities or liquidity needs or can be accessed by the business owner later for retirement income.

Business Owners / High Income Executives

As an entrepreneur, you have built a successful company but need an insurance solution that does more than just provide a death benefit. The cash value growth and tax benefits of an IUL policy can help you supplement retirement income, fund business opportunities, and transfer wealth.

The benefits unique to IUL make it a powerful financial vehicle for entrepreneurs looking to protect their business interests and provide for their families. The guarantees, tax advantages, and flexibility warrant a close look for business owners seeking solutions that do more than just provide a death benefit.

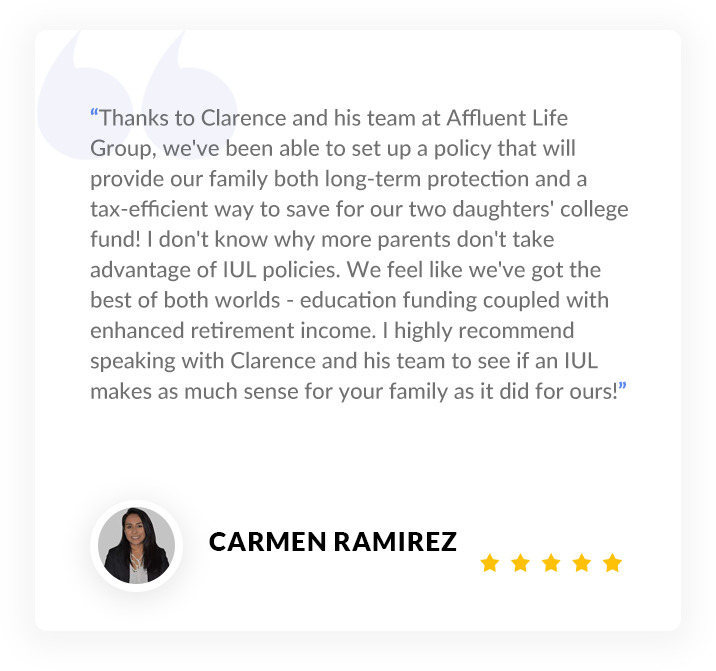

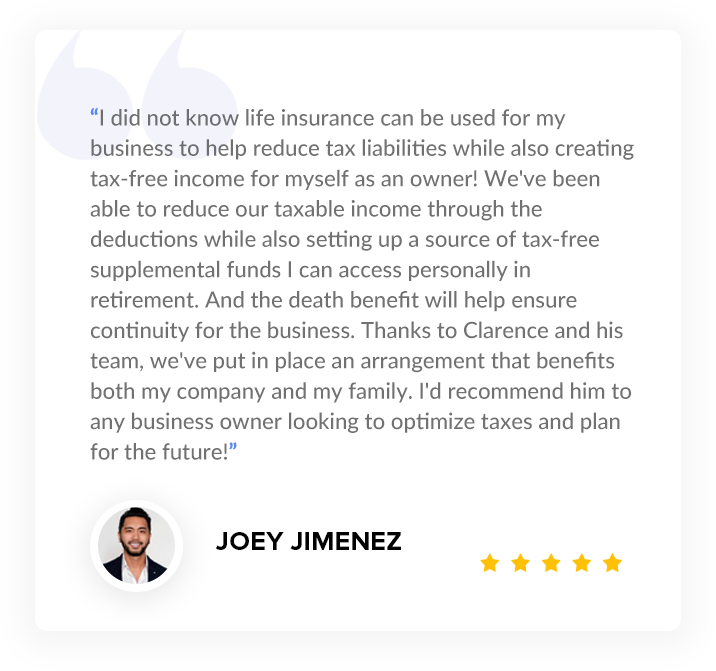

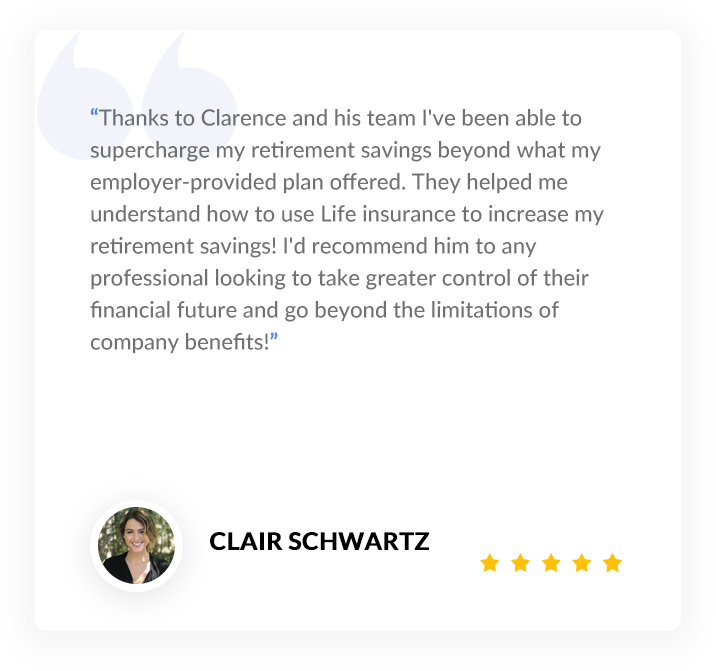

Hear From Our Clients

With over 3000+ satisfied clients, we are proud of providing excellent service

Our A+ Rated Partners

More questions? We have answers.

Life insurance can be complicated. Luckily, we're always here to help FAQS

Let's stay in touch

Get access to the latest in financial planning and personal finance insights.

© 2023 Affluent Life Group | All Rights Reserved

*Projected Results are Estimates Only and Not Guaranteed. Tax-Advantage Private Savings Account are Based on Using an Indexed Universal Life Insurance Policy With an Assumed Average Annual Return of 6.28% and Participating Loan Rate of 4%. Additional Policy Underwriting May Be Required to Achieve Projected Results. Costs of Insurance and Policy Expenses are Taken from a State Approved Illustration and Are Based on a Similarly Aged Male at a Preferred Health Rating. Estimated Cash Value and Income Results May Vary Based on Actual Gender, Age, and Approved Health Rating.

Past performance does not guarantee future results. There is no guarantee that any investment strategy or account will be profitable or will not incur loss. Investors should consider the investment objectives, risks, charges and expenses that make up this investment strategy carefully before investing. Investing involves risk, including the possible loss of principal. Share price, principal value, and return on investments will vary, and you may have a gain or a loss when you sell your investment.

Individuals affiliated with this broker/dealer firm are either Registered Representatives who offer only brokerage services and receive transaction-based compensation (commissions), Investment Adviser Representatives who offer only investment advisory services and receive fees based on assets, or both Registered Representatives and Investment Adviser Representatives, who can offer both types of services. Registered Representative offering securities through First Allied Securities, Inc. Member FINRA/SIPC.

All Content on this site is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in the Site constitutes professional and/or financial advice, nor does any information on the Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. Affluent Life Group is not a fiduciary or registered investment advisor. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other Content on the Site before making any decisions based on such information or other Content. In exchange for using this website (affluentfg.com), you agree not to hold Affluent Life Group, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision you make based on information or other Content made available to you through the Site.

This site is not a part of the Facebook website or Facebook Inc. Additionally, this site is not endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.