Better To Be Ten Years Early Than

One Minute Too Late

Educate - Understand - Service

Your family is our family

At Affluent Life Group, our mission is to educate and protect families by helping them financially prepare for life's uncertainties. As founders who grew up in challenging financial circumstances, we understand firsthand the grief and stress of losing a loved one without proper financial planning in place. Families should not have to resort to GoFundMe campaigns, fundraising events, and crippling debt just to honor their loved ones with a respectful goodbye.

Through our own experiences, we realized the power of life insurance and financial preparedness in transforming an unexpected loss from a moment of hardship into a time of remembrance and celebration. Now, with over 15 years of experience in the insurance industry, our team is dedicated to guide families through these difficult times by making sure their futures are protected.

We know there are a lot of misinformation out there when it comes to life insurance and financial planning. Not just life insurance but how to effectively use all these tools for financial planning, like tax-free savings. These misinformation is due to many people not knowing how to properly use them, or structure them, depending on their financial goals and needs. Which is why here at Affluent Life Group, our top priority is education first. We want to equip you and your family with the knowledge to be able to help yourself secure your financial goals. Done for you and work with you!

Our core philosophy is to provide excellent consultative guidance to understand each family's unique situation and goals. We aim to educate on all options so families can make informed decisions to secure their financial futures. At the end of the day, we view our clients as family, and take pride in delivering customized solutions so they have one less thing to worry about. Our mission is supporting families before, during, and after life's hardest moments.

What is life insurance?

Put simply, this financial tool lets you pass on money to your family tax-free when you die. For example, you could give $500,000 to your children tax-free to pay off debt or start a business after you pass away.

The reality is that we will all die eventually. Wealthy people plan ahead so they can protect the money they leave behind. But many folks wait until the last minute. Then they can't get or afford life insurance to create this kind of legacy or worst yet they can't get approved because of life illnesses.

Don't let that happen to you! Start planning now and use this tax-free wealth transfer tool. It lets you secure for your family's financial future when you're gone.

What are the different types of insurance?

There are two main types of life insurance: Term Life Insurance and Permanent Life Insurance

Term Life Insurance:

Covers your life and ensures you for 10-30 years of your life.

Imagine Term Life Insurance as if you are renting an apartment. Let’s say you pay rent to live in the apartment, you’re covering your shelter during that time. It's the same principle with Term Life Insurance.

Permanent Life Insurance:

In simple terms, it’s permanent and it last your life time!

Now unlike Term Life Insurance that expires, Permanent Life Insurance policies grows cash value tax-free. You secure your life and build cash value as a tax-free savings with potentially better returns than a normal savings account.

The cash value portion of your policy grows and participates in the performance of a stock market index, like the S&P 500 but without risk. It has downside protection from losses from the market performance. Rest knowing that you can grow your cash value without risk and have protection that last your entire life.

Our experienced financial professionals will help you pick the life insurance type that best fits your needs and budget. We'll guide you through your choices so you get the right policy.

What are living benefits?

All policies we help our clients with have "living benefits" feature. This allows you to access part of the death benefit while you are still alive if you get very sick.

For example, let's say your policy has a $500,000 death benefit.

And you were diagnosed with a chronic, critical or terminal illness; depending on the severity of the illness, you will be able to get $250,000 paid out to you or more.

This can help pay you for medical bills, replace income and other expenses if you were dealing with illnesses like stroke, cancer and heart attack.

The "living benefits" payout that you take out if you were to get sick would be subtracted from your original death benefit and if you were to die, they would pay the rest of the death benefit to your beneficiaries. But it gives you an option to tap into the policy value if you critically need the money.

How much does life insurance cost?

The cost of Term Life Insurance varies based on several factors. This includes your age, health, habits lifestyle and the amount and type of coverage you need. A healthy 30-year-old might pay as little as $20 per month for a Term Life Insurance policy, while an older person that is less healthy could pay several times that amount.

The cost of a Permanent Life Insurance policies, which provides coverage for the duration of your life and often includes a savings component that grows tax-free, can be significantly higher than the cost of a Term Life Insurance policy.

This is often why most of our clients schedule and claim their free consultation to have an in depth guidance. Our experienced financial professionals can properly structure their Permanent Life Insurance policy for the least cost of insurance and more cash value savings growth.

It is important to consider not only the cost of life insurance, but also the level of protection it provides and your unique needs and circumstances. Our experienced financial professionals can help you determine the most cost-effective options for your specific needs and provide a quote or illustration on performance if it's a permanent life insurance policy.

How much life insurance do I need?

The amount of life insurance you need depends on several factors. This includes your income, debts, assets and the number of people you want to protect. A general rule is to purchase coverage equal or up to 10-12 times your annual income. However, this may not necessarily be the right amount for your specific situation.

When deciding how much life insurance is best for you, you need to look at your long-term financial goals life: paying off debt, home purchase, businesses, retirement savings, college funding for your kids and to making sure your family has financial support after you are gone. We understand that this can be sensitive topics to talk about, that is why it is our responsibility as fiduciaries to guide you in the process with utmost respect, professionalism and care.

We understand the importance of building relationships and that our clients' life circumstances can change over time. That is why we often offer our clients a one free annual consultation to make sure they are up to date with their policies or if there is ever a need to change their policies to suit their lifestyle and new financial goals.

Still Figuring Out This

Life Insurance Thing?

Take a break and enjoy a relaxing cup of tea or coffee. There's no need to spend your precious weekend researching. I'll walk you through all the key information you need to know in a straightforward and easy-to-understand way, long before your drink grows cold.

Why Work With Our Experts

We have a team of licensed and experienced financial professionals in all 50 states who follow a three step formula:

Free Consultation:

We’ll start by having a simple conversation and ask you a couple of questions to better understand your situation, needs, and most importantly your financial goals for you and your family.

Catering Plans for You:

By asking about your financial situation - including goals, debt, and who you want to protect - we can recommend the right insurance amount. This ensures you get the coverage you need without being underinsured or overpaying. We then put together a plan that is completely made for you.

Fiduciary Responsibility:

We work with you by helping you create a monthly budget for insurance. Then we compare policies from 35 insurance companies to find the one that best fits your budget and needs.

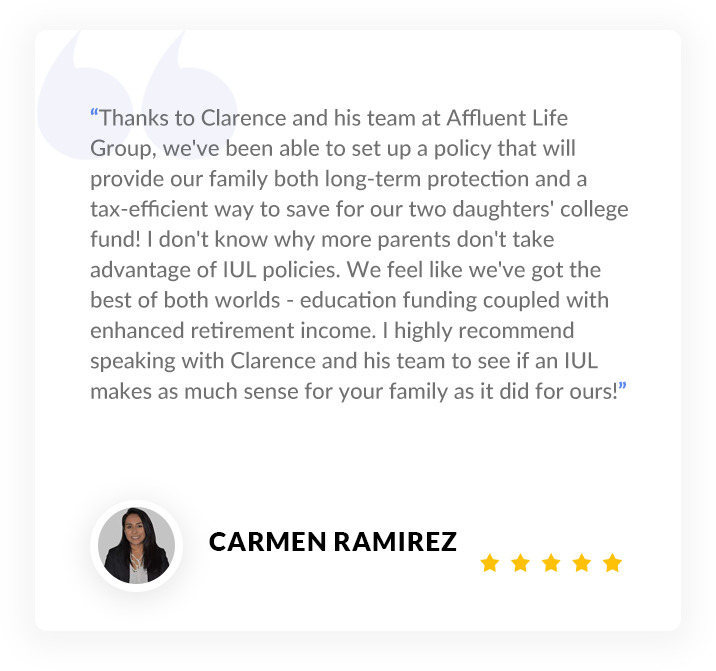

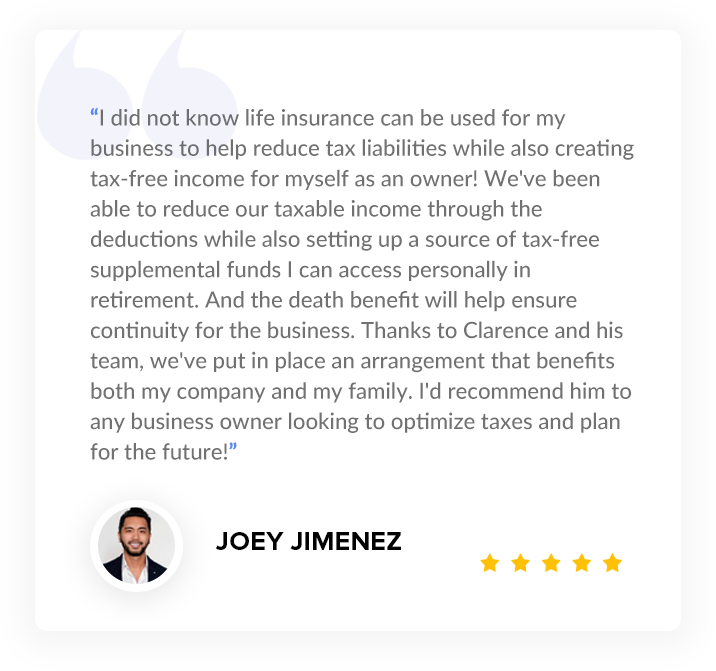

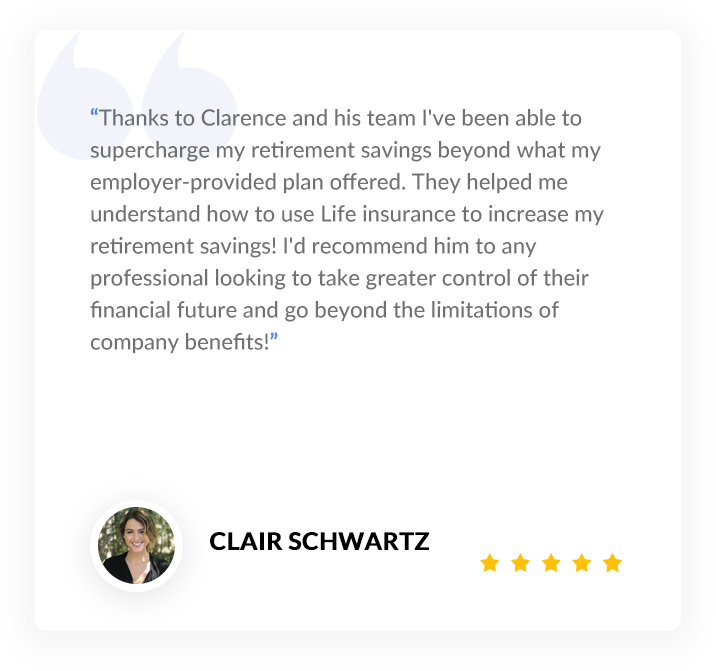

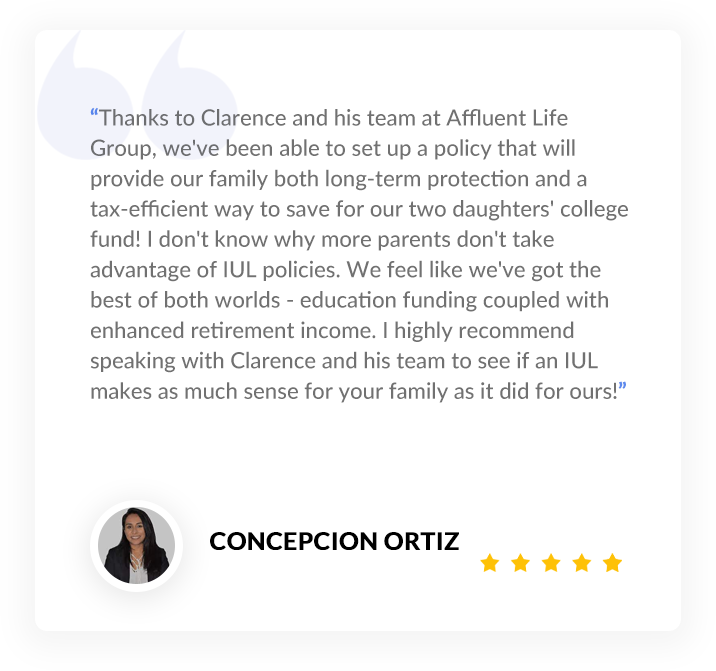

Hear From Our Clients

With over 3000+ satisfied clients, we are proud of providing excellent service

Our A+ Rated Partners

Let's stay in touch

Get access to the latest in financial planning and personal finance insights.

© 2023 Affluent Life Group | All Rights Reserved

*Projected Results are Estimates Only and Not Guaranteed. Tax-Advantage Private Savings Account are Based on Using an Indexed Universal Life Insurance Policy With an Assumed Average Annual Return of 6.28% and Participating Loan Rate of 4%. Additional Policy Underwriting May Be Required to Achieve Projected Results. Costs of Insurance and Policy Expenses are Taken from a State Approved Illustration and Are Based on a Similarly Aged Male at a Preferred Health Rating. Estimated Cash Value and Income Results May Vary Based on Actual Gender, Age, and Approved Health Rating.

Past performance does not guarantee future results. There is no guarantee that any investment strategy or account will be profitable or will not incur loss. Investors should consider the investment objectives, risks, charges and expenses that make up this investment strategy carefully before investing. Investing involves risk, including the possible loss of principal. Share price, principal value, and return on investments will vary, and you may have a gain or a loss when you sell your investment.

Individuals affiliated with this broker/dealer firm are either Registered Representatives who offer only brokerage services and receive transaction-based compensation (commissions), Investment Adviser Representatives who offer only investment advisory services and receive fees based on assets, or both Registered Representatives and Investment Adviser Representatives, who can offer both types of services. Registered Representative offering securities through First Allied Securities, Inc. Member FINRA/SIPC.

All Content on this site is information of a general nature and does not address the circumstances of any particular individual or entity. Nothing in the Site constitutes professional and/or financial advice, nor does any information on the Site constitute a comprehensive or complete statement of the matters discussed or the law relating thereto. Affluent Life Group is not a fiduciary or registered investment advisor. You alone assume the sole responsibility of evaluating the merits and risks associated with the use of any information or other Content on the Site before making any decisions based on such information or other Content. In exchange for using this website (affluentfg.com), you agree not to hold Affluent Life Group, its affiliates or any third party service provider liable for any possible claim for damages arising from any decision you make based on information or other Content made available to you through the Site.

This site is not a part of the Facebook website or Facebook Inc. Additionally, this site is not endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.